Fight Banking Discrimination Against Sex Workers

Sex workers and sex industry businesses in Australia face widespread discrimination on the part of banks.

On This Page

What Exactly is Being Refused to Sex Workers?

All business banking services can and often are refused, including:

- basic business debit accounts, basic transaction accounts, business debit cards

- merchant facilities (EFTPOS, Credit card facilities etc.)

- business loans

- mortgages on property where the business is located

- personal loans

Lack of access to basic banking services is not based on credit risk or other individually assessed financial risk. It is based on occupation or industry type.

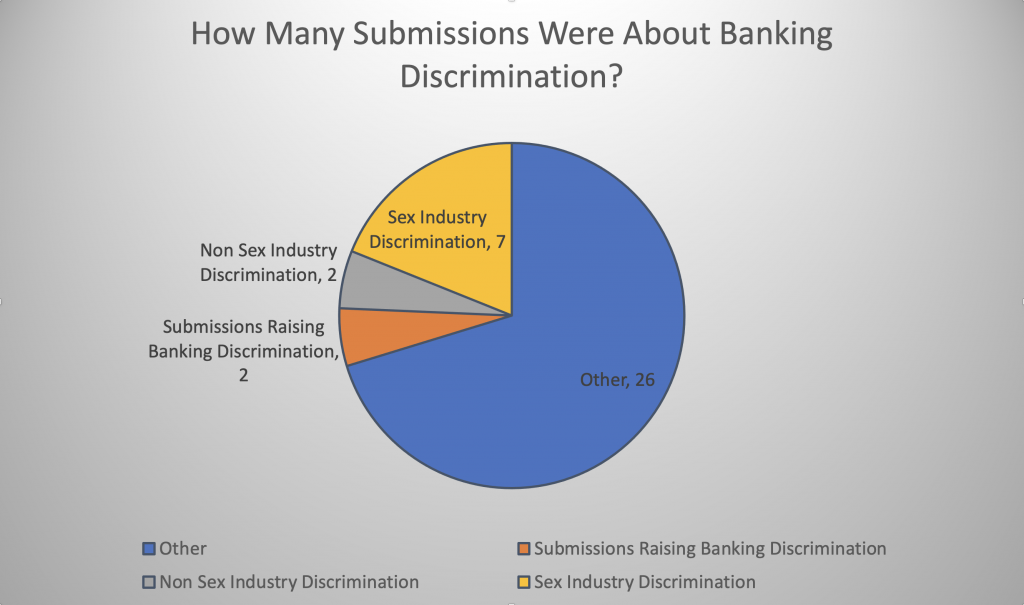

Existing Australian banking regulation does not protect customers from discrimination on the basis of occupation or industry type. However, in 2021 banking regulation was reviewed with a Final Report published in November 2021. A number of sex workers and sex industry businesses made submissions to the 2021 Banking Code Review. This type of banking regulation review only occurs every 3 years.

Discrimination against sex workers has never been raised in previous reviews.

On 28 July 2022, Sex Work Law Reform Victoria delivered a speech alongside porn performer Christine McQueen about financial discrimination against sex workers. The event was hosted by Humanists Victoria.

Watch the event on Youtube.

Banking Code Review Updates

On 6 December 2022, the Australian Banking Association (ABA) formally responded to all 116 recommendations made by the Banking Code Review. No recommendation can be implemented without the approval of the ABA. 16 of the 116 recommendations were relevant to sex workers, with the ABA refusing to accept the key recommendation about de-banking. We break down the key recommendations relevant to sex work and what the Australian Banking Association says about each one.

Recommendations relevant to sex work and small business are 23 (ePayment Code), 35-40 and 42-44 (accessible banking for vulnerable customers), 58 (debanking), 64, 66, 67, 69 and 71 (small business banking).

The most significant recommendation was number 58, which asks banks to give customers an opportunity to be heard and fix problems before their accounts are closed. The ABA refused to accept this recommendation.

No. | Recommendation | ABA Response |

| 58 | A customer should not be denied a banking service, or have an account closed, without the bank raising it with the customer and giving the customer an opportunity to respond, where consistent with AUSTRAC guidance. If the service is denied, or account closed, the bank should give a reason, where appropriate. Such decisions should be on a case-by-case basis. The BCCC should consider undertaking an inquiry into banks’ performance in accordance with these commitments. | Recommendation not supported at this point in time. |

23 | ABA banks should commit to subscribing to the ePayments Code and complying with the consumer protections in the ePayments Code. | Recommendation supported. |

35 | The Code should adopt the UK Financial Conduct Authority’s definition of a vulnerable customer – ‘someone who, due to their personal circumstances, is especially susceptible to harm- particularly when a firm is not acting with appropriate levels of care’. While some customers may be more likely to be vulnerable, it is important for banks to be alert to the circumstances of each and every customer in identifying vulnerability. | Recommendation supported in part. |

36 | The specific circumstances of customers who may be vulnerable listed in Clause 38, and the groups of customers listed in Clause 32 as a focus for inclusive banking services, should specifically state that the list ‘includes but not limited to’. | Recommendation supported. |

37 | The examples of groups of vulnerable customers in the Code should include people in prison (and those in transition) to bring attention to a group currently under recognised. | Recommendation supported in part. |

38 | The commitment in Clause 32 to provide banking services which are inclusive of all people, should be extended to provide that the vulnerabilities of both individuals and small businesses should be taken into account. | Recommendation not supported. |

39

| The wording in Clause 38 that the bank ‘may only become aware of your circumstances if you tell us’ should be removed and replaced with wording along the lines of Clause 93 in the 2020 General Insurance Code. Similarly, the wording in Clause 43 that the bank ‘may become aware if you are a low-income earner only if you tell us about it’ should be amended. While customers should be encouraged to tell their bank if they are a low- income earner, banks should commit to proactively identify customers who may be eligible for basic accounts. | Recommendation supported in part. |

40

| Following on from Recommendation 8, banks should commit to periodically auditing the effectiveness of staff training and systems for identifying vulnerable customers. | Recommendation supported in principle. |

| 42 | Clause 40 should be amended to include that if a vulnerable customer tells their bank about their personal or financial circumstances, subject to the customer’s agreement, the bank will record this information so as to minimise the number of times the customer has to provide this information. | Recommendation supported in principle. |

| 43 | The commitment in Clause 41 should be ‘to make it easier’ for a vulnerable customer to communicate with their bank, rather than ‘to try and make it easier’. | Recommendation not supported. |

| 44 | There should be a commitment that the bank will keep a vulnerable customer’s information secure and confidential | Recommendation supported. |

| 64 | Part 6 should be extended from referring to ‘lending to small business’ to cover ‘providing banking services to small business’. The first commitment in this part should be for banks to assist small businesses with their banking services that are suitable to their circumstances. | Recommendation supported in part. |

| 66 | To help clarify what parts of the Code apply to small business, and to recognise there is a difference in the requirements for lending to small business and lending to individuals, the references to small business lending in Part 5 should be shifted to part 6 of the Code. | Recommendation supported in part. |

| 67 | The Code should specify that future earning capacity is taken into account when assessing a small business’s capacity to repay a loan. | Recommendation supported in part.

|

| 69 | Banks should advise a small business if there is likely to be a delay in the initial indication of how long it would take for a decision, the reason for the delay, and give an estimate when a decision is likely. | Recommendation not supported.

|

| 71 | Banks should commit to tell small business the reason, if appropriate, as to why a loan was declined, along with what would be needed for the application to be reconsidered. | Recommendation supported in part. |

In November the 2021 Banking Code Reviewer, Mike Callaghan, published his Final Report.

The report takes the issue of sex industry discrimination seriously, making numerous recommendations about how the Code could be improved to better protect sex workers. The report contains an entire chapter, ‘Customers denied banking services’ on page 101, which finds that;

‘Banks should not have a ‘blanket’ denial of banking services on the basis that they are concerned that the Anti Money Laundering provisions may come into play….This is a major issue for legal businesses denied banking services. The Code should include a provision that a customer will not be denied banking services, or have an account closed, without the bank first raising it with the customer and giving the customer an opportunity to respond.’ ⁷

The Banking Code of Practice applies to 21 of Australia’s largest banks, including the Big Four banks.

Your Questions Answered

Any reference to small business is relevant to sex work and the sex industry. The Terms of Reference lay out what the Review wants people to write about in their submissions. The part of the Terms of Reference which most relates to the sex industry is clause 3 of the Scope, which reads:

‘The extent to which the Code contributes to banking services being inclusive, affordable and accessible for all customers, including: small business customers….’

The Review is looking at improving the Banking Code of Practice, which does not require banks to be inclusive and accessible for sex workers and small businesses more generally. The part of the Banking Code of Practice which most relates to the sex industry is Chapter 13, in Part 4 on page 21 of the Code. Chapter 13 does not currently refer to small business. Including small business in this Chapter would require banks to be inclusive and accessible to small businesses.

While most sex workers in Victoria are unable to work within the licensing system of sex work laws, it now appears that the Victorian may decriminalise sex work, with the media reporting a sex work decriminalisation bill is expected to be tabled by the end of 2021. Banks are only supposed to offer banking services to lawfully operating businesses. This means decriminalising sex work in Victoria would enable far more sex workers to apply for business bank accounts.

The Banking Code of Practice (The ‘Code’) is Australia’s primary form of banking regulation, requiring banks to treat their customers fairly. The Code applies to sole traders and small businesses operating Australia wide, not just in Victoria. The Code treats private sex workers and larger brothels and escort agencies in the same way – as ‘small businesses’.

The Code is enforced by the Australian Financial Complaints Authority (AFCA), which publishes almost all of its determinations (rulings).

Read AFCA determination on dispute between NAB and an escort agency

The Code is reviewed every 3 years, with the latest review concluding in November 2021 with the publication of the Final Report.

The Banking Code of Practice applies to 21 of Australia’s largest banks, including NAB, Commonwealth Bank, Westpac and ANZ. Payment processor companies, like Stripe, Square Payments and PayPal are not covered by the Code as they are not banks. Banks which are bound by the Code are the 21 members of the Australian Banking Association (ABA), a large organisation which represents the interests of its member banks.

The 21 member banks of the Australian Banking Association covered by the Code are:

AMP Bank | ANZ | Arab Bank Australia | Bank Australia |

Bofa Securities | Bank of China | Bank of Queensland | Bank of Sydney |

Bendigo and Adelaide Bank | Citigroup | Commonwealth Bank of Australia | HSBC |

ING Bank | Macquarie | MUFG | |

MyState Bank | NAB (bans all sex industry businesses) | Rabobank | Suncorp |

United Overseas Bank | Westpac |

Even though the Code doesn’t apply to some smaller banks in Australia, or to payment processor companies, the Code’s influence is significant. It is used as a general guide by other companies to how they ought to treat their customers.

The existing accessibility protections in the Code currently only apply to ‘customers’ (non business account holders), not ‘small businesses’, referred to as ‘inclusive and accessible banking’, see Chapter 13 of the Code.

Overall, the Code applies to individual non-business customers, sole traders (self-employed businesspeople such as private sex workers) as well as small businesses (such as escort agencies and brothels), but the existing accessibility protections contained within it only applies to customers. Both sex industry businesses (brothels and escort agencies) and private sex workers are considered to be ‘small businesses’ in the Code. This distinction is important, because the Code treats small businesses differently from other types of customers. Sex workers, including private sex workers, are classified as small businesses. Small businesses generally use business banking services.

There are legitimate reasons why banks can refuse to provide services to a sole trader or small business. One reason is if the bank has reason to believe a particular business is operating illegally. A belief that a business is operating illegally should be based on evidence not prejudice. This is why all states and territories in Australia urgently need to fully decriminalise all forms of sex work, so that sex workers can operate lawfully.

Technically, no. The Code does not refer to discrimination, it refers to ‘inclusive and accessible banking’ for vulnerable groups of ‘customers’. It does not provide for inclusive and accessible banking for sex workers, sex industry businesses and small business in general.

‘Chapter 13 Being inclusive and accessible’ requires member banks to be inclusive of:

- older customers

- people with a disability

- Indigenous Australians, including in remote locations

- people with limited English

Chapter 13 makes no reference to small business, occupation or industry type. This means the existing Code makes no requirement for banks to be inclusive and accessible for sex workers, sex industry businesses or small businesses more generally.

Banking discrimination can be addressed in a number of ways. State/territory anti-discrimination laws and federal banking regulations play different but important roles in tackling this systemic problem.

Anti discrimination laws don’t protect sex workers in all states. Sex workers’ rights activists, including SWLRV, are fighting to strengthen these laws.

Anti-discrimination cases can be difficult to prove and are very rarely used in the context of sex work, as they often require paying expensive lawyers to support tribunal legal action. This contrasts with large banks, which have billions of dollars to spend on lawyers to defend their discriminatory positions.

Breaches of the Banking Code of Practice are easier to enforce as investigations and public determinations (rulings) are conducted by the Australian Financial Compliance Authority (AFCA), at no cost to the sex worker.

The existing Banking Code of Practice puts the onus on sex workers to prove, in a tribunal using anti-discrimination laws, that discrimination has occurred. Strengthening the Code to require banks to be inclusive and accessible for small businesses will put the onus on the banks to demonstrate to the Australian Financial Complaints Authority (AFCA) that they are being inclusive and accessible for small businesses, as required by the Code.

An independent reviewer Mike Callaghan AM PSM conducted the review, publishing his Final Report in November 2021.

Mr Callaghan has a background in Australian and international financial regulation. Mr Callaghan is independent and does not work at the Australian Banking Association or any of its 21 member banks. Banking Code Reviews occur every three years.

On 6 December 2022, the Australian Banking Association responded to all 116 recommendations in the final report. The timeline⁸ for amending the Code is in 2023.

New code takes effect (including Pottinger Review changes) 1 January 2023 or 6 months after ASIC notifies its approval of the Code (whichever is the later).

Banking Code Review and Sex Work in the Media

Done by Law is a community radio show on Melbourne station 3CR. Hosted by lawyers, on 3 August 2021 the show interviewed sex worker Dean Lim and banking legal expert Professor Denis Nelthorpe.

Dean spoke about the reasons sex workers are so reluctant to engage openly with banks, and Denis provided a background on how banks discriminate against groups of banking customers, including people who have used marijuana and those working in the rock music industry. Access the podcast via Apple Podcasts at the link below.

In Ya Face is one of the longest running queer radio shows in Australia and has been on-air since 1992. On 6 August 2021, the show interviewed sex worker Dean Lim about the banking discrimination and the Banking Code Review. On the Apple Podcast episode below, Dean is interviewed in the first 14 minutes of the show.

Australia’s banks are the guardians of moral society. Yep, we kid you not by Tony Jaques for Crikey.com.au. Article is behind a paywall.

Fact Checking By Banking Lawyer

Professor Denis Nelthorpe AM has checked for the legal accuracy of this webpage regarding the current law, the Banking Code of Practice, and the Banking Code Review 2021. Professor Nelthorpe is a former board member with the Financial Ombudsman Scheme and a member of the Code Compliance Committee – Victorian LPG Industry. This is general information only and is not to be taken as legal advice. In the 1980’s, Professor Nelthorpe supported sex workers via workshops he delivered to the Prostitutes Collective of Victoria.

-

-

- See page 37 of the 2021 Independent Review of Banking Code of Practice CONSULTATION NOTE, July 2021 which reads ‘Consultation will include a public submissions process.’

- See definition of “You” on page 11 of the Banking Code of Practice

- See definition of “Small Business” on page 12 of the Banking Code of Practice

- See submissions by National Shooting Council, ASBFEO, SIFA, Assembly Four, Sex Work Law Reform Victoria, Victorian Pride Lobby, Eros, Queensland Adult Business Association, Queensland Government Prostitution Licensing Authority, Working Man and Dean Lim.

- See submissions by Assembly Four, Sex Work Law Reform Victoria, Eros, Queensland Adult Business Association, Queensland Government Prostitution Licensing Authority, Working Man and Dean Lim.

- See Chapter 2 of the INDEPENDENT REVIEW OF THE BANKING CODE OF PRACTICE 2021 INTERIM REPORT

- Mike Callaghan, Independent Review of the Banking Code of Practice (Final Report, November 2021) 102.

- See page 4 of the Banking Code of Practice Independent Review 2021 Terms of Reference

-

Sex Work/Sex Industry Submissions

Read Sex Work Law Reform Victoria’s submission

Read Eros submission

All submissions

What’s in the final report?

The Final Report, published in November 2021, is 179 pages long, covering all aspects of banking self regulation. The main section which applies to sex workers is on page 100 titled ‘Customers Denied Banking Services’. The following recommendations also relate in some way to the issue of sex industry discrimination: 23, 35, 36, 38, 40, 45, 58, 64, 66, 100, 101, 110.

The report recommends amendments to the Banking Code of Practice to ensure banks treat sex workers as individuals, rather than applying blanket bans on all sex workers. There are also recommendations about affording sex workers due process, an opportunity to respond when their accounts are closed, and, where possible, banks should notify customers of the reasons why their accounts have been closed. To quote from the section on page 100 titled ‘Customers Denied Banking Services’.

‘A customer should not be denied a banking service, or have an account closed, without the bank raising it with the customer and giving the customer an opportunity to respond, where consistent with AUSTRAC guidance. If the service is denied, or account closed, the bank should give a reason, where appropriate. Such decisions should be on a case-by-case basis. The BCCC should consider undertaking an inquiry into banks’ performance in accordance with these commitments. The Code should include a provision that a customer will not be denied banking services, or have an account closed, without the bank first raising it with the customer and giving the customer an opportunity to respond.’

© Sex Work Law Reform Victoria 2022

Last updated: 16 December 2022